Updated for the May 12, 2026 Federal Budget This update includes important information for anyone interested in the intersection of Gig worker and housing issues in Australia.

If you drive for rideshare platforms, freelance, or run a sole-trader business, you already know the hurdles of getting a mortgage without standard PAYG payslips. Historically, many self-employed Australians have relied on property investment—specifically negative gearing and the capital gains tax (CGT) discount—to build the wealth that traditional employer-paid superannuation usually provides.

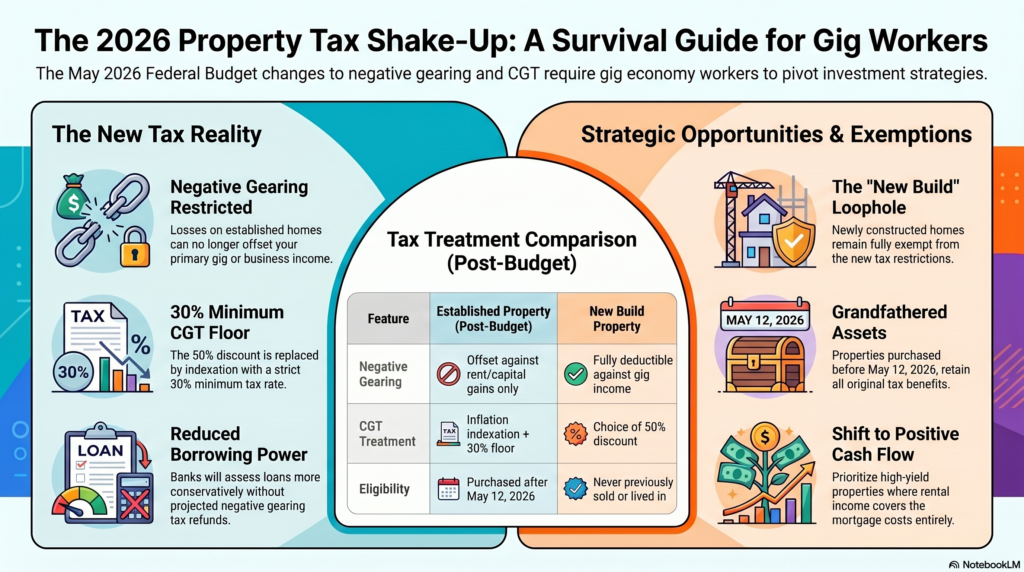

However, Treasurer Jim Chalmers’ Federal Budget, handed down on May 12, 2026, fundamentally changed the rules of property investing in Australia. Here is exactly what gig economy workers and self-employed borrowers need to know about the new landscape.

🔑 Key Takeaways (TL;DR)

- Negative Gearing Abolished for Established Homes: If you buy an existing (established) property after 7:30 PM on May 12, 2026, you can no longer use rental losses to reduce your taxable gig or business income. This rule officially takes effect on July 1, 2027.

- The 50% CGT Discount is Gone: From July 1, 2027, the 50% capital gains tax discount is being replaced by an inflation-adjusted indexation model with a minimum 30% tax rate on capital gains.

- New Builds are the Exception: The government desperately wants housing supply. If you invest in a newly constructed property, you are completely exempt from these changes—you can still negatively gear against your income and access the old CGT discount rules.

- Existing Portfolios are Safe: Properties you already owned or had under contract before Budget night are grandfathered in under the old rules.

How Does the New Negative Gearing Rule Affect My Gig Income?

Under the old rules, if the cost of holding your investment property (mortgage interest, strata, maintenance) was higher than the rent you received, you could deduct that loss against your primary income. For a freelancer with high taxable earnings, this was a massive tax shield.

Following the May 2026 budget, that tax shield is gone for established properties.

Losses on established homes can now only be offset against residential rental income or future capital gains from rental properties—not against your rideshare earnings, freelance invoices, or small business income.

What this means for you: You can no longer rely on property tax deductions to lower your end-of-year tax bill and free up cash flow. If you buy an older apartment, you have to ensure your business generates enough standalone cash to float any shortfall between the rent and the mortgage.

What Do the 2026 Capital Gains Tax (CGT) Changes Mean When I Sell?

The budget completely overhauled how your profits are taxed when you sell an investment property.

Previously, if you held a property for more than 12 months, you only paid tax on 50% of the profit. Starting July 1, 2027, the government is reverting to an “indexation” model. This means you will only be taxed on your real capital gain (the profit adjusted for inflation), but you will face a strict minimum 30% tax rate on those gains.

What this means for you: If your gig income fluctuates and you were planning to sell a property during a “low income” year to take advantage of a lower marginal tax bracket, that strategy is severely impacted. The 30% floor means the ATO gets its cut regardless of how little you earned from your business that year.

How Will This Impact Your Borrowing Power as a Self-Employed Worker?

Banks assess self-employed borrowers heavily on serviceability—your proven ability to repay the loan based on your business’s cash flow.

In the past, mortgage brokers could factor your projected negative gearing tax refunds into your serviceability calculation, effectively boosting your borrowing power. Because those tax refunds will no longer exist for established properties, banks will assess your loan application much more conservatively. Your alt-doc or low-doc loan application will now rest almost entirely on the strength of your Business Activity Statements (BAS) and your last two years of tax returns.

Alternative Property Strategies for Freelancers and Gig Workers

Key Takeaways

- The May 12, 2026 Federal Budget changed property investing rules for gig workers in Australia, impacting negative gearing and capital gains tax.

- Negative gearing for established homes is abolished starting July 1, 2027; tax deductions from rental losses can no longer offset gig income.

- The 50% capital gains tax discount is replaced by a minimum 30% tax rate on profits, affecting gig workers’ selling strategies.

- Investing in new builds remains exempt from the new rules, allowing negative gearing and the old CGT discount to apply.

- Existing properties purchased before the budget are grandfathered under the old rules, maintaining their tax benefits for gig workers.

While the 2026 budget closed several doors, it purposefully left one wide open. If you are self-employed and want to invest, here is how you can pivot:

- Pivot to New Builds: The government made newly constructed homes fully exempt from the tax shake-up to encourage building. If you buy a new build, you can still negatively gear the losses against your gig income, and you keep the choice of using the traditional 50% CGT discount.

- Chase Positive Cash Flow: Instead of buying premium properties that run at a loss for the tax benefits, self-employed buyers should look to regional areas or high-yield property types where the rent covers the mortgage from day one.

- Hold Existing Assets: If you bought an investment property before May 12, 2026, do not panic sell. Your property is grandfathered under the old rules, making it a highly valuable asset in your wealth-building portfolio.

🙋 Frequently Asked Questions (Gig Workers & 2026 Property Laws)

Can I still claim property maintenance and real estate agent fees as tax deductions?

Yes. The 2026 budget changes do not stop you from claiming standard holding costs (like repairs, strata, council rates, and management fees) against your rental income. The change only means that if those costs exceed your rental income (creating a net loss), you can no longer deduct that shortfall against your primary gig or freelance income if it is an established property.

Does the 2026 budget change how banks calculate my gig income for a home loan?

The budget doesn’t legally dictate bank lending policies, but it directly impacts them. Because you can no longer rely on negative gearing tax refunds to boost your cash flow on established homes, lenders will scrutinize your standalone Business Activity Statements (BAS) and ABN income much more closely to ensure you can service the loan on your own.

What classifies as a “new build” to get the negative gearing exemption?

To qualify for the new build exemption, the property generally must be brand new and never previously sold or lived in as a residential dwelling. Buying off-the-plan, purchasing a newly constructed house-and-land package, or building a new dwelling on vacant land will all allow you to retain the old negative gearing and CGT discount rules.

I bought an investment property in 2024. Do these new tax rules apply to me?

No. Any investment properties purchased before the budget was handed down at 7:30 PM on May 12, 2026, are entirely grandfathered. You can continue to negatively gear your losses against your gig income and utilize the 50% capital gains tax discount when you eventually sell.

Table of contents

- 🔑 Key Takeaways (TL;DR)

- How Does the New Negative Gearing Rule Affect My Gig Income?

- What Do the 2026 Capital Gains Tax (CGT) Changes Mean When I Sell?

- How Will This Impact Your Borrowing Power as a Self-Employed Worker?

- Alternative Property Strategies for Freelancers and Gig Workers

- 🙋 Frequently Asked Questions (Gig Workers & 2026 Property Laws)