TL;DR: How Outlook Finance helped a self-employed business owner with a complex 6-company structure bypass traditional bank rejections. They unlocked $500,000 in equity using low doc alternative documentation.

It is a common and incredibly frustrating scenario for self-employed Australians: you have a thriving business, ambitious plans for expansion, and a property sitting on a goldmine of equity. But when you approach your everyday bank for a capital injection, your application is rejected. This happens simply because your paperwork doesn’t fit neatly into their standard boxes.

At Outlook Finance, we specialize in finding solutions when traditional lenders close their doors. Recently, we helped a self-employed client navigate this exact hurdle. We turned a stressful bank rejection into a half-a-million-dollar win to fuel their business growth.

The Challenge: Complex Structures and Missing Financials

Our client possessed fantastic entrepreneurial drive and had been trading successfully for five years. They wanted to tap into their existing property’s equity to fund a major business expansion. However, when they approached their current bank, the application stalled immediately.

Here is what we were up against:

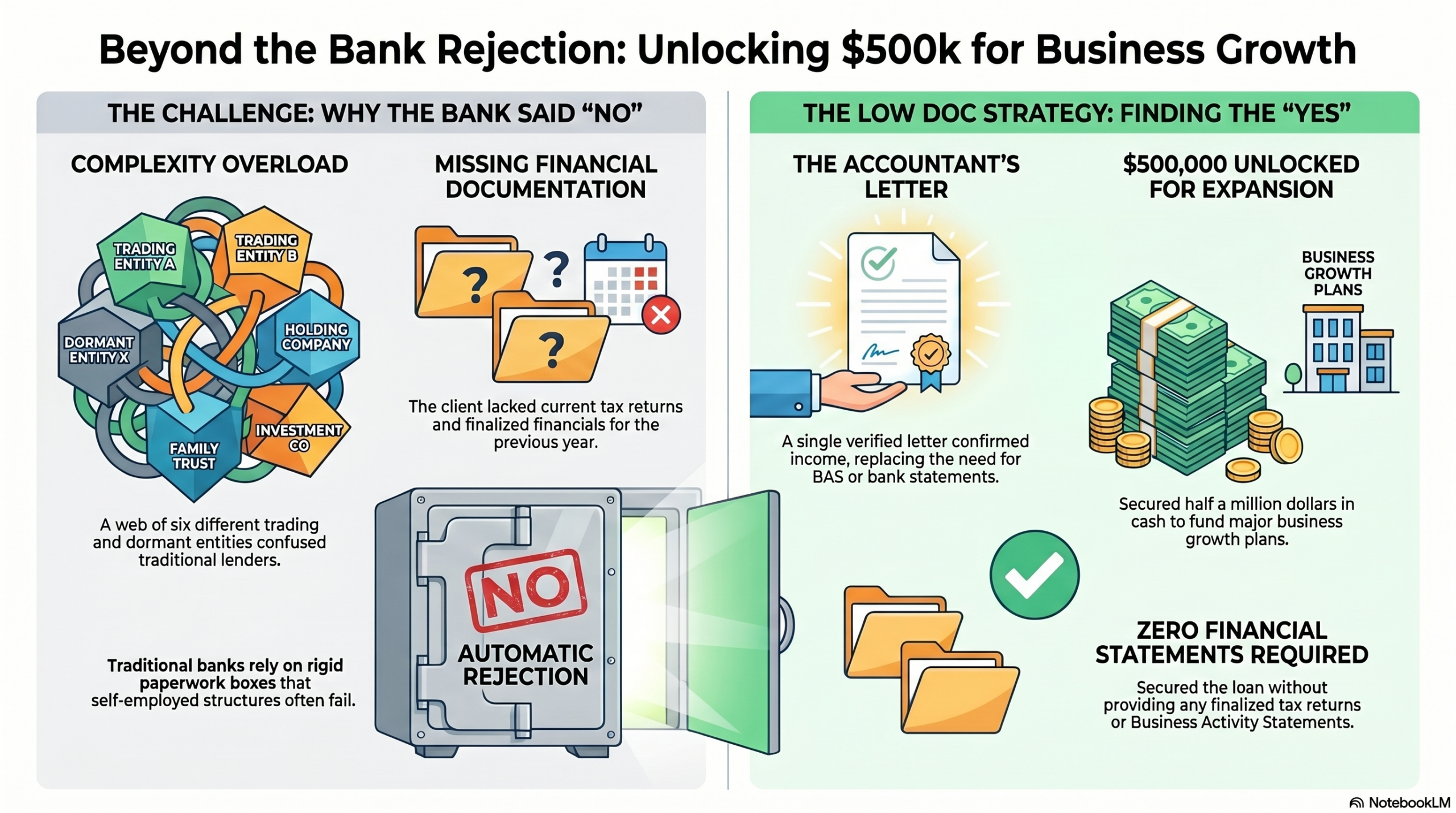

- A Complex Corporate Structure: The client operated a web of six different companies. Four were dormant (non-trading). One was a brand-new venture (only trading for six months), and one was their primary, established entity (trading for five years).

- Incomplete Paperwork: Their accountant had not yet prepared the finalized financial statements for the previous tax year.

- The Bank’s Reaction: Traditional banks rely heavily on up-to-date, finalized tax returns and straightforward company structures to assess risk. For the major banks, this scenario was deemed “too complex.” Without the latest financials, it resulted in an automatic decline.

The Strategy: Alternative Documentation (Low Doc)

We knew the client’s primary business was strong, cash-flowing, and that they had substantial equity tied up in their real estate. They didn’t need to wait months for their accountant to finalize their tax returns. Instead, they just needed a lender who understood complex, self-employed setups.

Instead of fighting a losing battle with standard banking policies, we pivoted to a Low Doc (Alternative Documentation) lending strategy.

Because we have access to a wide network of specialist non-bank lenders, we were able to present the client’s true financial position. We did this without relying on traditional “full doc” requirements.

The Result: $500,000 Unlocked with a Single Letter

We bypassed the traditional red tape entirely. By understanding the client’s actual serviceability, we achieved an outstanding outcome:

- Zero Financial Statements Required: We secured the loan without needing to provide any bank statements, Business Activity Statements (BAS), or finalized tax returns.

- The Power of an Accountant’s Letter: We utilized a single, verified letter from the client’s accountant. This declaration confirmed their income and their comfortable ability to service the new loan.

- Debt Consolidation & Cash Out: We successfully refinanced all of their existing business loans to streamline their ongoing debts. At the same time, we unlocked $500,000 in cash.

This capital was injected straight into their business, allowing them to execute their expansion plans immediately rather than waiting until the next financial year.

Key Takeaways

- Self-employed Australians often face bank rejections due to complex business structures and incomplete financial paperwork.

- Outlook Finance helps clients navigate traditional banking hurdles using alternative documentation (Low Doc) lending strategies.

- A client with six companies unlocked $500,000 in equity without needing finalized financial statements or bank documents.

- Instead, a verified letter from the client’s accountant confirmed their serviceability, allowing for swift capital release.

- If you’re self-employed and face barriers from banks, consider reaching out to specialists who understand alternative lending options.

Estimated reading time: 7 minutes

Table of contents

Frequently Asked Questions (FAQ)

Q: What exactly is an “Accountant’s Letter” and why do lenders accept it? A: An accountant’s letter is a formal declaration signed by your registered accountant certifying your current business income and confirming that you can afford the proposed loan repayments. Specialist non-bank lenders accept this because they understand that past tax returns don’t always reflect a business’s current cash flow or true financial strength.

Q: Will my complex company structure (multiple entities, family trusts) disqualify me? A: Not with the right lender. While traditional banks rely on automated systems that automatically reject complex setups, specialist lenders assess applications manually. They understand how holding companies, family trusts, and dormant entities work, and they won’t penalize you for having a sophisticated business structure.

Q: Do I need a massive amount of equity to do a cash-out refinance? A: For low doc loans, lenders generally prefer a Loan-to-Value Ratio (LVR) between 60% and 80%. This means you typically need to leave at least 20% to 40% equity in the property. The exact amount depends on the lender, the location of the property, and the strength of your application.

Q: Are the interest rates significantly higher if I don’t provide tax returns? A: Low doc interest rates are generally slightly higher than standard “full doc” rates because the lender takes on more risk by not requiring comprehensive financials. However, many self-employed borrowers use this as a short-term strategy to access capital immediately. Once your tax returns are finalized, we can often look at refinancing you back to a standard, lower-rate loan.

Q: How fast can a low doc loan be approved compared to a traditional bank loan? A: Because there is less paperwork to process (no need to analyze years of tax returns, BAS, or bank statements), specialist lenders can often move much faster than traditional banks. Depending on the complexity of your situation, approval and settlement can happen in a matter of weeks, getting the capital into your hands sooner.

Could Your Property Equity Be Working Harder For You?

If you are self-employed, an intricate business structure or a delay in your tax returns should not lock you out of accessing your own wealth.

If you have equity available in residential or commercial property that could be better allocated to grow your business, consolidate debt, or invest in new opportunities, you need a broker who understands how to navigate alternative lending.

Don’t let a bank’s “no” stop your business growth. Reach out to the specialist team at Outlook Finance today to explore your low doc loan options.

Low Doc Home Loans – Outlook Finance

How to Unlock Your Property Equity Without Tax Returns

If you are self-employed and need capital to expand your business, consolidate debt, or invest, waiting for your tax returns to be finalised isn’t your only option. Here is a step-by-step guide on how to leverage your equity using a low-doc strategy.

Step 1: Calculate Your Available Equity Before applying for any loan, you need to know how much equity you actually have.

- The Formula: Current Property Value – Current Mortgage Balance = Total Equity.

- Usable Equity: Lenders generally allow you to borrow up to 80% of your property’s value (known as an 80% LVR). So, calculate 80% of your property’s estimated value, then subtract your current mortgage balance. This is roughly the “usable” cash you can unlock.

Step 2: Check Your ABN Registration Non-bank lenders require proof that your business is established and stable.

- Ensure your Australian Business Number (ABN) has been active for at least 12 to 24 months.

- If your turnover requires it, ensure your GST registration is also up to date.

Step 3: Have a Conversation with Your Accountant If you are bypassing traditional tax returns, your accountant becomes your best asset.

- Discuss the Accountant’s Letter strategy with them. You will need them to sign a declaration confirming your current income. They should also verify that your business generates enough cash flow to comfortably afford the new loan repayments.

Step 4: Clean Up Your Credit File Because specialist lenders are taking on more risk by not looking at full financial statements, they rely heavily on your credit history.

- Ensure you have no recent defaults or late payments on credit cards, car loans, or your current mortgage. A clean credit file significantly boosts your chances of approval.

Step 5: Partner with a Specialist Mortgage Broker Approaching a standard bank with a low-doc application will almost certainly result in a rejection.

- Contact a specialist broker like Outlook Finance. We have access to the specific non-bank lenders who offer these alternative documentation loans. We will assess your complex company structure and package your application. Then we present it to the lender most likely to say “yes.”

Step 6: Get Your Property Valued Once we submit your application, the lender will order an independent valuation of your property to confirm the equity you want to access is actually there. If the valuation comes back strong and the accountant’s letter checks out, your funds can be unlocked. Then they can be transferred to your business accounts.